Jan 26, 2015

Volatility Views 143: The Great Fed Debate

Volatility Review: The week in volatility

- ECB takes all of the vol out of the market in one fell swoop. S&P 500 volatility streak longest since '12 as 1% moves multiply. The S&P 500 Index rose 0.5 per cent yesterday and moved 1.3 per cent from its lowest to highest levels.

- VXST: Another week of crappy volume. (The Mystery of Short-Term Volatility)

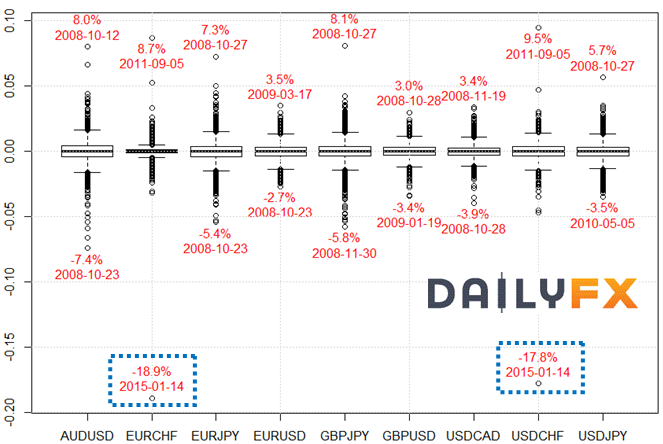

- FX Volatility: Another crazy week following the Swiss Franc crisis.

- Crude Oil: Crude continues to take it on the chin. Domestic crude supplies at near record levels. Iraq increasing production to offset declining revenues. Death of the Saudi King adding to the confusion.

Here’s the chart that Mark was referring to from Daily FX:

Volatility Voicemail: Listener questions and comments

- Question from Marcus N - You discussed the retracement from backwardation to contango in VIX Futures on the last episode. If I thought the retracement would be rapid and I wanted to play that retracement, would the near-term futures or options be my best bet?

- Question from Avrile - Risk premium - What is it? I have seen it defined many ways. Is it a products 30-day implied vs. 30-day realized? 10-day vs. 10-day? If using 30-day realized that’s a lagging indicator. Do you then have to extrapolate that forward using an algorithm, then compare that to 30-day implied to get a more accurate number? What about comparing something like front month or 30-day implied SPX volatility vs VIX Cash or VIX Future? Is that the best surrogate for the markets risk premium? Or has VIX Cash become such a polluted number that it is better to stick with straight SPX implied volatility?

Crystal Ball: Mark and Jared prognosticate wildly!